Equities fell in the first quarter after two consecutive years of gains exceeding +20%. The year started off strong, with the S&P 500 reaching a new all-time high in mid-February. However, sentiment shifted late in February amid rising policy uncertainty in Washington, and the broad market index finished the quarter down.

Developments in Washington took center stage in Q1 as the Trump administration started rolling out its policy agenda. Their early efforts focused on trade policy, tariffs, and reducing government spending. These policies are a notable shift from the status quo and have drawn attention from investors and business leaders due to their potential impact on the economy. The uncertainty surrounding these policies led to a spike in market volatility. This volatility is likely to remain elevated until there is greater clarity as to the effects of these policies. Furthermore, consumer sentiment continued to decline, with negative expectations around inflation mirrored in the Fed’s Summary of Economic Projections released at the March meeting.

The quarter’s fall in the equity market can be traced to the divergence between earnings estimates and valuations. Two prominent measures are analysts’ profit expectations for the upcoming year and price-to-earnings ratios, or how much investors are willing to pay for those future earnings. Earnings estimates tend to be less volatile than P/E ratios, which is natural as the market often swings between optimism and pessimism. As sentiment shifted over the course of the first quarter from optimism to a more cautious tone, valuations declined even as future earnings estimates largely remained on course.

Performance

Most of the equity market declines occurred in the second half of the quarter, after the S&P 500 set an all-time high in February. The sell-off was driven by a small group of mega-cap stocks, and their size and weight within broad market indices impacted performance trends. Market leadership shifted and last year’s top performers lost momentum. Last year, the “Mag-7” (Alphabet, Amazon, Apple, Meta, Nvidia, Microsoft, Tesla) delivered an impressive 63% return, which carried the broader market to a +23% gain. In contrast, the equal-weight S&P 500 gained only 11%. YTD, the biggest stocks are now dragging the market down. The Mag-7 has declined roughly 15% through March-end while the equal-weight S&P 500 is down approximately 1%.

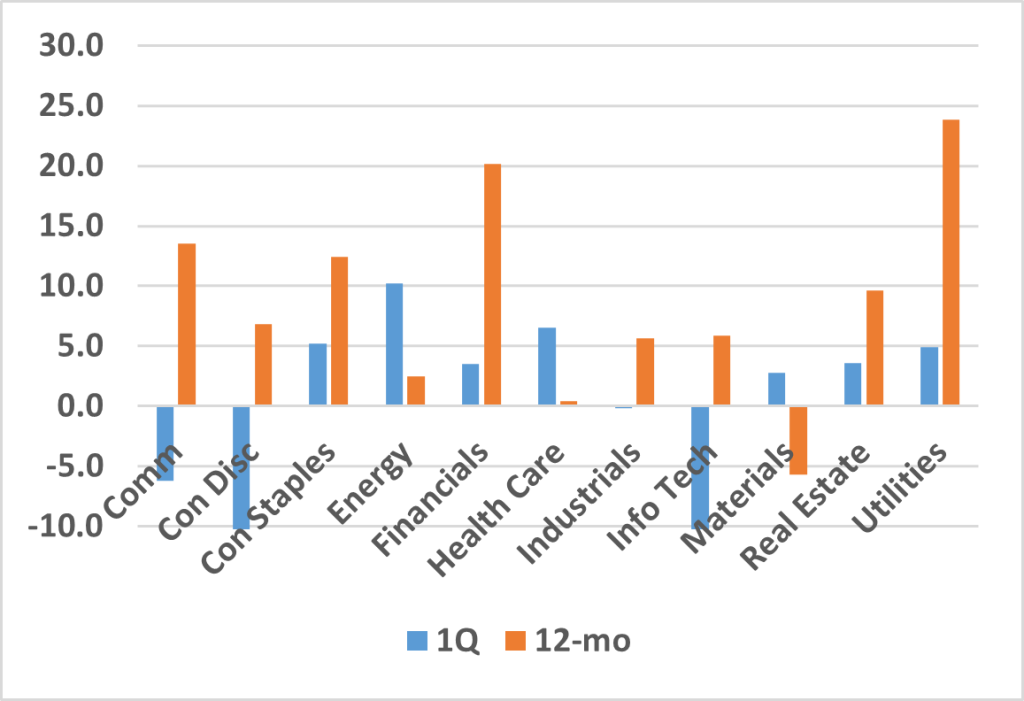

From a style perspective, the first quarter saw a swing from growth-oriented stocks to value. Sectors such as energy (+10.2%), health care (+6.5%), consumer staples (+5.2%), and utilities (+4.9%) outperformed. Growth stocks fell out of favor for reasons mentioned above as investors moved to those companies whose cash flows are steadier and more predictable. Sectors that lagged all others include consumer discretionary (-13.8%), information technology (-12.7%), and communication services (-6.2%). Small- and mid-cap equities were also negative during the quarter with the Russell 2000 Index down 9.5% and the Russell Mid-Cap Index falling 3.4%.

S&P 500 Sector Performance

International

Global equity markets experienced notable developments during the first quarter, with international equities delivering solid returns despite geopolitical turbulence. The MSCI EAFE rose by 6.86%, underscoring broad-based optimism in key regions though substantial challenges remain.

Germany-based equities rallied following that country’s announcement that a one-trillion Euro defense and infrastructure plan had been approved. The plan marks a pivotal shift from the country’s historically cautious fiscal approach. Other equity markets in the region rallied on the prospect of overall higher spending, even as bond markets reflected unease over the prospect of ballooning deficits. The degree to which other countries across Europe follow Germany’s lead remains to be seen.

Chinese equities also performed well supported by advancements in AI technology. The nation’s new platform, DeepSeek, demonstrated its ability to rival U.S. innovations at substantially lower costs. Despite this development, challenges persisted. Domestic consumption remained sluggish, and structural concerns in the real estate sector and adverse demographic trends continued to weigh on the outlook. Elsewhere in Asia, results were varied. Japan’s equity markets remained flat while Australia and India posted modest declines. Australian equities struggled due to falling commodity prices, a sector vital to the country’s economy. India contended with slower consumer and government spending and a deceleration in IT sector hiring.

Though non-US markets displayed resilience, developments in the U.S. significantly impacted global sentiment. The U.S. economy faced its first quarterly equity market decline since 2023, with tariffs announced by President Trump which created uncertainty. The ensuing change in sentiment weighed on the U.S. dollar, which fell unexpectedly, likely reflecting broader market concerns.

Commodities

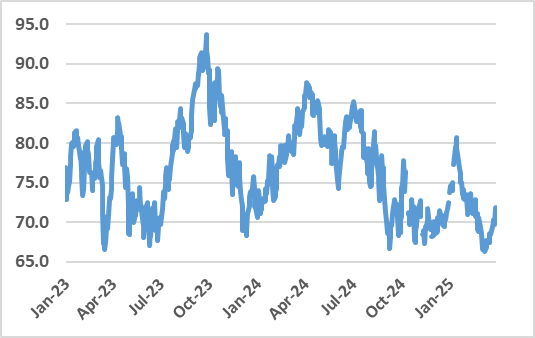

The broad commodity market posted positive returns in March and delivered positive returns for the first quarter despite tariff headlines generating volatility across the asset class. The Bloomberg Commodity Index was up 7.74% for the quarter. Underlying subsectors showed mixed returns for March, led by precious metals (+9.6%). Gold continued its run, posting a monthly gain of 9.5%, benefitting from a weaker U.S. dollar and a bid for safe-haven assets. Energy also posted positive returns with both Brent crude and WTI crude rising. The petroleum complex reversed course from earlier in the quarter in response to lower production from OPEC countries. Industrial metals also moved higher, particularly copper, as investors rushed to get exposure ahead of announced tariffs expected to take effect in April. Agricultural products fell 2.0%, with cocoa dropping 13.4%. Wheat declined 3.4%, impacted by the threat of retaliatory tariffs.

Crude Oil Prices – WTI

Fixed Income

The Bloomberg US Aggregate Index returned 2.78% in the first quarter, marking the best start to a calendar year since 2023. The January momentum was quickly derailed by a combination of the release of DeepSeek’s AI model, questioning the sustainability of the tech market run of the previous two years and even more so by the disruptive impact of potential tariffs.

As the quarter progressed, volatility in the U.S. Treasury market became the name of the game as the markets reacted to economic news about inflation, consumer sentiment, the labor market, and the implementation/cancelation/re-introduction of tariffs. The yield on the 10-year finished only slightly lower in January, while February saw the yield compress 33 basis points to 4.21% as the aforementioned concerns grew and investors sought the safety of Treasuries.

Another notable theme during the quarter was credit spread expansion. Credit spreads measure the difference between high-yield corporate bonds and safer government bonds. Spread levels can serve as a real-time gauge of market sentiment, showing how easy or expensive it is for companies to borrow money. A narrower spread signals that investors view credit as low risk, while a wider spread signals higher perceived default risk. While still narrow by historical standards, the first quarter saw a fairly significant widening of these spreads, indicating an increased level of caution on the part of investors.

Inflation

The Federal Reserve remained squarely on the sidelines as inflation proved stubborn during the quarter and the labor market continued to show strength. The federal funds rate remained in the 4.25%-4.50% range, and the Fed used its two Q1 meetings to reinforce its data dependency approach. The FOMC’s “dot plot”, which is followed by many market participants, indicated expectations of two 25-bps rate cuts by year-end. Fed Chair Powell cited the uncertainty surrounding the implementation of tariffs on the U.S. and global economies as one of the reasons for holding steady on rates.

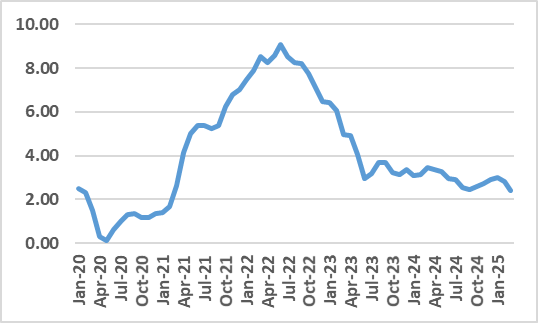

Core inflation reports during the quarter were a bit of a rollercoaster, starting the year at 3.2%, peaking at 3.3% in January, before reversing course in February and March and finishing the quarter at 2.8%. Considering that this measure is backward looking, they do not reflect the potential effect of any tariffs. The labor market began on a slower note relative to the end of 2024 yet averaged 152,000 jobs added per month during the quarter. While the tariff question led in the headlines, data regarding the consumer moved to the forefront with historically poor readings on everything from consumer confidence to inflation expectations. The University of Michigan Consumer Sentiment Index, which collects consumer attitudes and expectations data, spent the first part of 2025 in a downward trend. The data further reflect that consumers’ expectations are for inflation to increase over the coming year.

Consumer Price Index – YoY Change

First Quarter & 2025 Insights

Market volatility can be unsettling, but it’s a normal part of investing. Periods of enthusiasm often lead to recalibration. It’s natural to feel uncertain, but history shows that staying invested through volatility and maintaining a longer-term perspective is the prudent approach.

Historical data shows that market drawdowns like the one experienced in the first quarter are not just common, they’re healthy and a recurring part of investing. While these corrections can be uncomfortable in the moment, they serve the important function of resetting valuations and curbing speculative excess. Without these occasional declines, markets could become dangerously overextended, increasing the risk of more severe and extended drawdowns.

Despite these frequent and sometimes severe drawdowns, the S&P 500 has delivered strong returns for nearly a century. This is despite wars, recessions, inflation spikes, financial crises, and a global pandemic. The upward trajectory is driven by economic growth, innovation, and corporate earnings growth. Volatility isn’t a sign that something is broken, it’s the price of admission to investing. Staying invested through the ups and downs has consistently been one of the most effective strategies for building wealth over time. Market declines can feel unsettling in the moment, but history shows the powerful effect of compounding returns over time.

Brian T. Moore, Vice President Trust Officer, Chesapeake Wealth Management

Published April 2025

References

1. S&P 500 Sector Return Data

2. Crude Oil Prices – WTI – Federal Reserve Economic Data: Year to date, crude oil prices, West Texas Intermediate.

3. CPI – Year over Year Change – Federal Reserve Economic Data: Year over year percentage change.

Disclaimer

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Chesapeake Wealth Management), or any non-investment related content, made reference to directly or indirectly in this newsletter, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Chesapeake Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his or her individual situation, he or she is encouraged to consult with the professional advisor of his or her choosing. Chesapeake Wealth Management is neither a law firm nor a Certified Public Accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Chesapeake Financial Group, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.

SEARCH

Welcome to the Login Menu.

You can access your account below.

It’s dependable and secure, and it will pop up in a new window in case you need to revisit the website.

We use information collected through cookies and similar technologies to improve your experience on our site, analyse how you use it and for marketing purposes.

We and our partners use information collected through cookies and similar technologies to improve your experience on our site, analyse how you use it and for marketing purposes. Because we respect your right to privacy, you can choose not to allow some types of cookies. However, blocking some types of cookies may impact your experience of the site and the services we are able to offer. In some cases, data obtained from cookies is shared with third parties for analytics or marketing reasons. You can exercise your right to opt-out of that sharing at any time by disabling cookies.

These cookies and scripts are necessary for the website to function and cannot be switched off. They are usually only set in response to actions made by you which amount to a request for services, suchas setting your privacy preferences, logging in or filling in forms. You can set your browser to block oralert you about these cookies, but some parts of the site will not then work. These cookies do not store any personally identifiable information.

Analytics

These cookies and scripts allow us to count visits and traffic sources, so we can measure and improve the performance of our site. They help us know which pages are the most and least popular and see how visitors move around the site. All information these cookies collect is aggregated and therefore anonymous. If you do not allow these cookies and scripts, we will not know when you have visited our site.

Embedded Videos

These cookies and scripts may be set through our site by external video hosting services likeYouTube or Vimeo. They may be used to deliver video content on our website. It’s possible for the video provider to build a profile of your interests and show you relevant adverts on this or other websites. They do not store directly personal information, but are based on uniquely identifying your browser and internet device. If you do not allow these cookies or scripts it is possible that embedded video will not function as expected.

Google Fonts

Google Fonts is a font embedding service library. Google Fonts are stored on Google's CDN. The Google Fonts API is designed to limit the collection, storage, and use of end-user data to only what is needed to serve fonts efficiently. Use of Google Fonts API is unauthenticated. No cookies are sent by website visitors to the Google Fonts API. Requests to the Google Fonts API are made to resource-specific domains, such as fonts.googleapis.com or fonts.gstatic.com. This means your font requests are separate from and don't contain any credentials you send to google.com while using other Google services that are authenticated, such as Gmail.

Marketing

These cookies and scripts may be set through our site by our advertising partners. They may be used by those companies to build a profile of your interests and show you relevant adverts on other sites. They do not store directly personal information, but are based on uniquely identifying your browser and internet device. If you do not allow these cookies and scripts, you will experience less targeted advertising.