Markets carried their strong momentum from Q2 into Q3, with the S&P 500, NASDAQ, and small-cap stocks each hitting new highs. Investor sentiment remained optimistic despite soft labor market data and mixed economic signals, and stocks traded higher due to strong corporate earnings, the Federal Reserve’s pivot toward rate cuts, and easing trade tensions. The technology sector remained an important contributor, as artificial intelligence companies reported strong earnings growth. At the same time, improving market breadth added fuel to the rally, and small-cap stocks finally broke above their 2021 highs.

The quarter opened on solid footing. Economic activity had recovered from the tariff-driven volatility earlier this year, and incoming data pointed to steady consumer and business demand. The stock market traded higher in July, driven by confidence that the economy could withstand high interest rates and trade uncertainty without slipping into recession.

By late summer, cracks began to emerge in the labor market. By August, the unemployment rate rose to 4.3% following two months of weaker job growth. While the labor data raised concerns about an economic slowdown, separate data showed consumer spending remained solid. Economic growth was still positive, but the economy was softening.

The shift in the economic backdrop was significant because it changed the conversation around Federal Reserve policy. As labor market data softened, the market adjusted its forecast to price in a more accommodative Fed and multiple interest rate cuts before year-end. In the market’s view, slowing job growth wasn’t a recession signal but rather a catalyst for the Fed to resume its rate cutting cycle. The question was when, not if, the Fed would deliver its next cut.

Performance

Artificial intelligence continued to be a top market theme during the quarter. An increased pace of technology-related investment is being directed toward high-performance computer chips, cloud architecture, data center construction, and the power and cooling needed to run it all. The spending boom has become a significant contributor to economic growth and helped offset softness in rate-sensitive areas such as housing, manufacturing, and non-AI business investment.

Stocks climbed to new highs in Q3, boosted by the Fed’s rate cut, resilient earnings, and continued enthusiasm for all things AI. The Fed’s rate cut marked a shift toward policy support and fueled optimism for a “soft landing”. The S&P 500 gained more than 8% during the quarter, bringing its year-to-date return to over 14%. Technology stocks remained a key driver, but broader market leadership also helped. Small-cap stocks rallied sharply in anticipation of the Fed’s rate cut. The Russell 2000 surpassed its previous high from 2021 and returned nearly 12% as investors bet that rate cuts would benefit small companies. In another sign of the market’s optimism, cyclical sectors broadly outperformed their defensive counterparts.

S&P 500 Sector Performance

International

The third quarter saw international stocks rise once again, with the MSCI EAFE Index increasing 5.5%, marking a third straight quarter of gains and a year-to-date increase of just over 25%.

Asian markets led during the quarter, with China and Japan contributing meaningfully. Chinese equities rallied on growing confidence that the country’s domestic producers are becoming less reliant on foreign suppliers, especially in important areas such as artificial intelligence. Japanese stocks advanced as governance reforms accelerated. The Tokyo Stock Exchange has pushed for better capital efficiency, leading to a new wave of parent-subsidiary buyouts that has turned policy talk into action. Meanwhile, European stocks saw modest but positive gains. Germany, which had been an outperformer earlier in the year, underperformed in Q3 as positive economic momentum slowed due to weakness in exports and uncertainty tied to new U.S. tariffs and EU exports.

Emerging markets generally benefitted from China’s rebound, with Mexico and Brazil outpacing the benchmark while Indian stocks declined amid tariff headlines, geopolitical headwinds and softer consumption trends.

With one full earnings season behind us post-Liberation Day, three themes are evident. First, companies are deferring some capital expenditures due to elevated uncertainty across global markets. Second, companies are contemplating changes to their production and assembly locations to adapt operations to a less globalized world. Lastly, companies are refining pricing, adjusting product sizing and leveraging technology to build resilience.

Looking out to Q4, global central banks remain broadly accommodative, which has created a supportive backdrop for equities. Inflation risk appears to be moderating around the globe, but concerns around growth continue to build. China’s stimulus continues to support near-term GDP growth, but year-over-year comparisons will become more difficult due to one-time purchases and tariff-related demand pull-forward. Japanese equities should continue to benefit from corporate governance reform; however, investors will be looking for tangible evidence of change before allocating capital given the country’s demographic challenges and a history of unrealized reforms. Europe is attempting to accelerate its own reforms to improve competitiveness, but high debt levels and political uncertainty in some countries raise questions about long-term sustainability.

Commodities

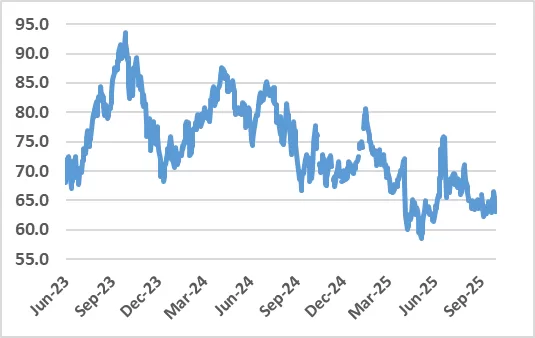

The Bloomberg Commodity Index rebounded in the third quarter, following a decline in the previous quarter. Precious metals led performance with gold and silver posting double digit gains. The Fed’s first interest rate cut of 2025 contributed to a weaker U.S. dollar, while concerns about the Fed’s independence and ongoing central bank gold purchases propelled the yellow metal to new all-time highs. Agricultural and industrial metals posted gains. Strength in coffee and livestock helped offset weakness in grains, while increases in aluminum and zinc partially mitigated declines in copper and nickel. Energy declined, driven primarily by continued weakness in natural gas. Temperate weather suppressed demand and elevated natural gas inventories, more than offsetting gains in crude oil and refined products.

Crude Oil Prices – WTI

Fixed Income

The Bloomberg US Aggregate Bond Index gained 2.0% for Q3 bringing YTD performance for the index up to 6.1%. The quarter saw several market-moving developments. Those included the long-delayed tariffs implemented in August, a labor market that began to show signs of weakness, a dovish shift from the Federal Reserve at Jackson Hole, and growing concerns of a government shutdown. As in Q2, risk assets have continued to shrug off economic and political headwinds, with investor demand keeping spreads near historically tight levels. Overall, the quarter reflected a market increasingly focused on central bank policy, with credit markets showing resilience despite mounting macroeconomic uncertainty.

The Federal Open Market Committee moved forward with the first adjustment to the Fed Funds rate since December 2024. As the committee stated, their action reflected a shift in the balance of risks with the downside risk to employment having risen. Inflation has ticked up since the spring; a trend acknowledged by the committee. This most recent cut was described as a “risk management cut” and expectations are for a meeting-by-meeting approach. The committee’s ongoing bias to ease was more apparent in the September Summary of Economic Projections, with the median projection for the Fed Funds rate at year end implying an additional 50 basis points of reduction over the two remaining meetings.

The Treasury yield curve had been in a bull steepening shift leading into Q3, with a more stabilized spread between shorter and longer yields over the past three months. A bull steepening of the curve occurs when short-term rates move lower (usually fueled by Fed rate cuts) but market concerns over longer term inflation and increased Treasury issuance pushes long-term rates higher. Since the beginning of the year, the spread between the 2-year and 10-year has grown from 0.33% to 0.54% while the spread between the 2-year and 30-year has jumped from 0.54% to 1.12%. While the Treasury market delivered positive performance during the quarter, it lagged both the corporate and securitized sectors and pulled the overall performance of the Bloomberg U.S. Aggregate Bond Index lower.

The investment grade corporate market posted its strongest quarterly return (+2.6%) since Q3’24, driven by spread tightening and strong investor demand. Except for the market disruption in Q2 around the announcement of tariffs, investment grade corporate spreads have continued to grind tighter throughout the year. Investors continue to look for opportunities in the investment grade corporate space while issuers flock to meet demand. Nearly $400 billion in new issuance during the quarter brings year-to-date issuance to $1.3 trillion, 3% ahead of last year’s pace.

The securitized market delivered another strong quarter of performance, returning 2.4%. The sector has consistently delivered strong quarter-over-quarter performance since the start of the year. Plain vanilla pass-through mortgage-backed securities led the way, generating a 2.4% return, followed closely by collateralized mortgage obligations (CMOs) which returned 2.3%. Commercial MBS and asset-backed securities were also positive on the quarter as spreads moved lower throughout the quarter.

Labor Market/Inflation Update

Recent reports of a resilient labor market may have overstated the underlying strength. According to the Bureau of Labor Statistics’ preliminary benchmark revision to March 2025 non-farm payrolls, total employment was 911,000 lower than previously reported. The revision implies an average monthly job loss of 76,000; a sharp contrast to previous estimates of growth. Collectively, the data suggests the recent slowdown follows a longer period of modest expansion, potentially justifying a more aggressive Fed easing cycle. The final benchmark revision is expected to be released in February 2026. In addition to the benchmark revisions, broader labor market indicators paint a picture of sustained weakness. The average monthly job gains in 2025 have been 102,000, well below monthly averages of the past two years. Despite the slowdown, unemployment remains well below the “natural level of unemployment”, though it should be noted that the past three months have seen an increase from 4.1% to 4.3% in August.

The Federal Reserve’s preferred measure of inflation, the core personal consumption expenditure (PCE), increased 2.9% compared to August 2024, in line with both market expectations and July’s reading. This marked the highest reading since February and was the fifth consecutive increase since April. The economic conundrum continues to plague the Federal Reserve – higher inflation requires higher rates, but a weaker labor market requires lower rates, and if both exist concurrently, which is more important to address? As mentioned above, the FOMC, at the moment, is prioritizing the labor market while tolerating modestly elevated levels of inflation.

Q4’25 Insights

The outlook for the economy is constructive heading into the final quarter of the year, although it may be uneven. Growth appears to be moderating, with softer labor market data offset by solid consumer spending. Investors will be watching closely to see whether the slowdown remains orderly or turns into something more disruptive. For now, the market views a “soft landing” as the base case, where the economy cools enough to ease inflation pressures without causing a recession. A sharp drop in either job growth or consumer spending would be enough to change the soft-landing narrative.

Federal Reserve policy will likely dominate headlines again in Q4. The September rate cut ended its 9-month pause, but policymakers have signaled a gradual easing cycle rather than an aggressive one. The market forecasts two more cuts by year-end, though this outlook could shift if inflation re-accelerates or the labor market stabilizes. In that sense, Q4 is set up to be a very data dependent quarter.

Corporate earnings will be another area of focus. Earnings have proven surprisingly resilient this year, with Q2 earnings season producing solid growth and a high beat rate despite tariff volatility and policy uncertainty. With Q3 earnings season underway, management guidance will be key as companies update investors on the impact of tariffs and their 2026 outlooks. Profit margins are likely to remain under scrutiny due to tariffs, economic uncertainty, and supply chain challenges.

As mentioned, AI-related investment remains a major theme. Companies are reporting unfilled orders stretching into 2026 and capex plans measuring in the hundreds of billions, reinforcing the view that AI will be a multi-year investment cycle. However, valuations for AI companies are expensive, and much of the backlogs and spending plans are widely known and already reflected in stock prices. An earnings disappointment or skepticism around AI economics could weigh on the technology sector’s leadership and, by extension, the broader equity market.

Brian T. Moore, Vice President Trust Officer, Chesapeake Wealth Management

Published October 2025

References

1. S&P 500 Sector Return Data

2. Crude Oil Prices – WTI – Federal Reserve Economic Data: crude oil prices, West Texas Intermediate.

Disclaimer

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Chesapeake Wealth Management), or any non-investment related content, made reference to directly or indirectly in this newsletter, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Chesapeake Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his or her individual situation, he or she is encouraged to consult with the professional advisor of his or her choosing. Chesapeake Wealth Management is neither a law firm nor a Certified Public Accounting firm and no portion of the newsletter content should be construed as legal or accounting advice.

We use information collected through cookies and similar technologies to improve your experience on our site, analyse how you use it and for marketing purposes.

We and our partners use information collected through cookies and similar technologies to improve your experience on our site, analyse how you use it and for marketing purposes. Because we respect your right to privacy, you can choose not to allow some types of cookies. However, blocking some types of cookies may impact your experience of the site and the services we are able to offer. In some cases, data obtained from cookies is shared with third parties for analytics or marketing reasons. You can exercise your right to opt-out of that sharing at any time by disabling cookies.

These cookies and scripts are necessary for the website to function and cannot be switched off. They are usually only set in response to actions made by you which amount to a request for services, suchas setting your privacy preferences, logging in or filling in forms. You can set your browser to block oralert you about these cookies, but some parts of the site will not then work. These cookies do not store any personally identifiable information.

Analytics

These cookies and scripts allow us to count visits and traffic sources, so we can measure and improve the performance of our site. They help us know which pages are the most and least popular and see how visitors move around the site. All information these cookies collect is aggregated and therefore anonymous. If you do not allow these cookies and scripts, we will not know when you have visited our site.

Embedded Videos

These cookies and scripts may be set through our site by external video hosting services likeYouTube or Vimeo. They may be used to deliver video content on our website. It’s possible for the video provider to build a profile of your interests and show you relevant adverts on this or other websites. They do not store directly personal information, but are based on uniquely identifying your browser and internet device. If you do not allow these cookies or scripts it is possible that embedded video will not function as expected.

Google Fonts

Google Fonts is a font embedding service library. Google Fonts are stored on Google's CDN. The Google Fonts API is designed to limit the collection, storage, and use of end-user data to only what is needed to serve fonts efficiently. Use of Google Fonts API is unauthenticated. No cookies are sent by website visitors to the Google Fonts API. Requests to the Google Fonts API are made to resource-specific domains, such as fonts.googleapis.com or fonts.gstatic.com. This means your font requests are separate from and don't contain any credentials you send to google.com while using other Google services that are authenticated, such as Gmail.

Marketing

These cookies and scripts may be set through our site by our advertising partners. They may be used by those companies to build a profile of your interests and show you relevant adverts on other sites. They do not store directly personal information, but are based on uniquely identifying your browser and internet device. If you do not allow these cookies and scripts, you will experience less targeted advertising.