After a volatile start to the year, the stock market staged a strong rebound over the last three months. In Q1, market sentiment was cautious due to rising policy uncertainty, concerns about slower economic growth, and questions about the longer-term outlook in the artificial intelligence industry. In Q2, caution gave way to renewed optimism as tensions eased, tariffs had a limited economic impact, and companies posted a stronger than expected Q1 earnings. The dramatic shift in sentiment across the quarters created two distinctly different market environments.

The first half of 2025 was busy and eventful, but for all that happened, markets ended the first half not far from where they started the year. The S&P 500 returned 6.1% through the end of June after being down over 15% at one point, and it trades at a similar valuation to the star of the year. Long-term interest rates, as measured by the 30-year U.S. Treasury bond yield, ranged from 4.40% to 5.10% but ended the first half of the year near 4.8%, where it started. For those not following markets closely, it might seem as though little has changed.

Up to this point, this year has been defined by large, frequent shifts in U.S. trade policy. There were periods of increasing tariffs and targeted actions against trading partners followed by exemptions and temporary agreements. While the first quarter was marked by trade escalation, the second quarter saw a significant shift toward de-escalation. Tariffs and trade policy uncertainty have also influenced Fed policy. The central bank has faced a difficult trade-off: tariffs that could lead to higher inflation that also have the potential to slow economic growth. Given this uncertainty, the Fed held interest rates steady in May and June, reiterating that it wants to see more data before considering further cuts.

Performance

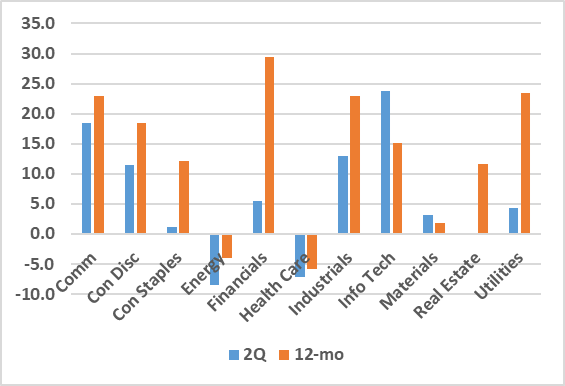

The escalation in the 1st quarter and de-escalation in the 2nd quarter created two distinct market environments. Low volatility stocks such as utilities, consumer staples, and healthcare performed well during the first quarter whereas more cyclical “high beta” stocks such as industrials, financials, and energy performed better in the second quarter. Equity market returns reveal a dramatic change in market leadership over the first half of the year. The S&P 500 rose 10.8% in Q2 after falling 4.3% in Q1, while the Russell 2000 (small-caps) gained 8.5% following a 9.5% drop. Growth and Tech stocks led the Q2 market reversal. The Russell 1000 Growth (large-caps) jumped 17.7% after a 10% Q1 decline, and the NASDAQ 100 gained 17.8% after an 8.1% loss. Defensive sectors that outperformed early in the year lagged as investors rotated toward riskier areas.

Despite the reversal from Q1 to Q2, one trend remained intact. International stocks outperformed U.S. stocks for a second straight quarter, with developing and emerging market stock indices both returning more than 11% in Q2. Year-to-date, developed and emerging market stocks have returned 20.2% and 16.4%, respectively, outperforming the S&P 500 by over 10%. Most of the outperformance can be attributed to a weaker U.S. dollar, which is being impacted by tariffs, policy uncertainty, and a rotation out of U.S. stocks into international stocks.

S&P 500 Sector Performance

International

International equity markets delivered a strong performance during the 2nd quarter with the MSCI ACWI ex-US advancing 12.0%. This performance came despite notable volatility stemming from geopolitical tensions and shifting global trade dynamics. Liberation Day, market by the President’s sweeping tariff announcement, initially sent global markets reeling. However, much of the anxiety quickly reversed as many of the proposed tariffs were either softened or delayed, allowing equity markets outside the U.S. to recover swiftly and ultimately deliver solid gains.

Geopolitical concerns cast a long shadow over markets throughout the quarter. Most prominently, the Israel-Iran conflict escalated into open conflict before a US-brokered ceasefire halted hostilities in late June. Oil prices spiked sharply during the height of tensions but settled as the truce took hold and diplomatic efforts resumed. The war in Ukraine also persisted with no clear path to resolution. While the direct market reaction to these conflicts was relatively contained, the broader uncertainty contributed to market volatility across regions.

Despite these challenges, several international markets showed notable resilience. Europe led the benchmark higher, buoyed by falling inflation expectations and a second consecutive rate cut from the European Central Bank. ECB President Christine Lagarde signaled that further easing may be off the table for now, as inflation has fallen below the central bank’s target rate of 1.9%. Alongside monetary policy, fiscal policy has taken center stage. NATO’s collective commitment to raise defense spending to 5% of GDP and new U.K. infrastructure plans injected fresh optimism, particularly in sectors related to industrials and construction.

In Japan, the story continues to be one of measured progress on corporate reform. A growing number of companies are increasing share buybacks and moving to consolidate parent-child share listings, steps that reflect ongoing improvements in shareholder alignment. China’s equity market remained flat for the quarter, weighed down by continued uncertainty regarding consumer demand and macroeconomic policy. While the U.S. and China agreed in May to a 90-day mutual tariff reduction, hoped for a broader breakthrough have since stalled. In contrast, South Korean equities rallied following the conclusion of their presidential election, which ushered in a period of relative political stability. In Latin America, several markets benefited from dovish central bank actions and favorable currency movements. Mexican equities gained on the back of interest rate cuts and a stronger peso, while Brazilian stocks were lifted by a combination of attractive valuations and renewed fiscal discipline.

Commodities

The commodity markets did not escape the effects of tariff-related volatility. The Bloomberg Commodity Index fell 3.0% during the 2nd quarter, reversing its 9.0% first quarter gain. Losses hit three of the four major sectors, those being energy, agriculture, and industrial metals. In energy, April’s tariff disruptions overshadowed a June rally sparked by Middle East tensions. Heating oil rose on supply concerns tied to potential disruption in the Strait of Hormuz. Natural gas gave up nearly all of its first quarter gains due to mild weather and high inventories. Agriculture declined on improved crop forecasts and higher output expectations. Conversely, soybean oil was boosted by proposed EPA biofuel mandates favoring domestic production. In the industrial metals space, aluminum rose on higher input costs, China’s policy support, and U.S. tariffs. Precious metals rose as investors turned to gold, copper, and silver amid the turbulence.

Crude Oil Prices – WTI

Fixed Income

The Bloomberg US Aggregate Bond Index gained 1.21% for the 2nd quarter bringing YTD performance for the index up to 4.02%. The story of the second quarter was all about the journey and not the destination, as the markets were roiled by higher-than-expected tariffs across the board. Fixed income markets followed a similar path as equities, dropping precipitously in the early days of April before rallying in the latter days of the quarter. Several factors contributed to the second quarter being more chaotic and unsettling than usual. Those being the aforementioned tariffs, crude oil price volatility driven by the Israel-Iran conflict, U.S. fiscal concerns highlighted by Moody’s finally downgrading U.S. credit quality to AA+ from AAA, and, finally, the ongoing demand for the resignation of Fed chair Jerome Powell.

It is well known that markets dislike uncertainty. Following the initial 10% across the board tariff announcement, the yield on the 10-year Treasury jumped 50 bps while the yield on the 30-year rose 46 bps. This disruption led to a 90-day pause, triggering a massive rally. As the quarter progressed, markets fell prey to every “Breaking News” flash, ranging from the “tit-for-tat” between the U.S. and China to rulings from the U.S. Court of International Trade. Contributing to the uncertainty was the news that Moody’s had finally joined S&P (2011) and Fitch (2023) in downgraded U.S. government debt from AAA to Aa1. Moody’s cited the government’s inability to agree on measures to reverse the trend of large fiscal deficits and ever-increasing interest costs. While the Federal Reserve largely remained on the sideline for the quarter in terms of monetary policy, Fed Chair Powell remained firmly in the crosshairs of President Trump. Though there have been continued calls from the President for Powell’s resignation and even discussions of replacing him prior to the end of his term, Powell has not seemed rattled. Afterall, monetary policy is determined by the twelve voting members of the FOMC and not by the Fed Chair themself.

While the Treasury market delivered a positive quarterly return, it lagged both the corporate and securitized sectors. The main reason for the lag in performance had to do with the twisting of the yield curve as the shorter end moved lower and the longer end pushed higher. This was the result of growing concerns over the fiscal environment. Similar to the Treasury market, the corporate bond market experienced significant fluctuations throughout the quarter yet ended June with spreads tighter than where they began. As a reminder, spread is the additional yield over similar duration Treasuries that compensates investors for additional credit risk. Despite the volatility throughout the quarter, investors continued to clamor for the sector as the overall yield it provides remains attractive.

2025 Second Half Insights

At the start of the year, few could have anticipated the events and market volatility that would unfold over the first six months. The market’s early year optimism was disrupted by policy driven volatility, a dynamic that could persist in the second half of the year. However, despite the policy uncertainty and market volatility, financial markets have proven resilient. During the 2nd quarter, the S&P 500 posted its strongest quarterly return sine the 4th quarter of ’23, fully reversing the 1st quarter sell-off.

The rebound suggests the market believes the economic impact of the tariffs will be modest and temporary. However, the economy is highly complex, and introducing trade policy volatility could have a range of impacts. Tariffs could be short-lived, causing only minor disruptions as businesses and consumers adjust. In contrast, the cumulative effects of trade policy uncertainty could start to weigh on the broader economy in the second half of the year, leading to slower economic growth, weaker labor demand, and higher inflation. For now, markets seem to be pricing in a blend of the two scenarios; expecting growth to moderate later this year while remaining cautiously optimistic that the long-term effects will be limited.

The coming months will provide important context, with economic data and earnings reports capturing a period marked by both trade escalation and de-escalation. Corporate earnings commentary will shed light on how trade developments have affected business conditions, and companies will provide earnings guidance for the coming quarters. Second-quarter GDP growth will be released in late July, offering insight into how shifting trade policy and tariffs have impacted the U.S. economy. Along the way, there will be more trade policy developments, along with monthly economic data releases to track tariffs’ impact on consumer spending, manufacturing activity, and the labor market.

Market volatility can be unsettling, but it’s a normal part of investing. Periods of enthusiasm often lead to recalibration. It’s natural to feel uncertain, but history shows that staying invested through volatility and maintaining a longer-term view is a prudent approach. By maintaining a diversified portfolio aligned with your long-term goals, you are best positioned to weather short-term market swings.

With uncertainty on the horizon, the theme for the second half is simple; focus on what you can control. It’s impossible to know what impact the tariffs will have on the global economy or whether the administration will change its mind once again. However, history shows the economy and market usually adapt to changing environments. Rather than reacting to headlines and market volatility, the best course of action is to stay focused on your financial plan, maintain a diversified portfolio, and make decisions in line with your long-term goals.

Brian T. Moore, Vice President Trust Officer, Chesapeake Wealth Management

Published July 2025

References

1. S&P 500 Sector Return Data

2. Crude Oil Prices – WTI – Federal Reserve Economic Data: crude oil prices, West Texas Intermediate.

3. CPI – Year over Year Change – Federal Reserve Economic Data: Year over year percentage change.

Disclaimer

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Chesapeake Wealth Management), or any non-investment related content, made reference to directly or indirectly in this newsletter, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Chesapeake Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his or her individual situation, he or she is encouraged to consult with the professional advisor of his or her choosing. Chesapeake Wealth Management is neither a law firm nor a Certified Public Accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Chesapeake Financial Group, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.

We use information collected through cookies and similar technologies to improve your experience on our site, analyse how you use it and for marketing purposes.

We and our partners use information collected through cookies and similar technologies to improve your experience on our site, analyse how you use it and for marketing purposes. Because we respect your right to privacy, you can choose not to allow some types of cookies. However, blocking some types of cookies may impact your experience of the site and the services we are able to offer. In some cases, data obtained from cookies is shared with third parties for analytics or marketing reasons. You can exercise your right to opt-out of that sharing at any time by disabling cookies.

These cookies and scripts are necessary for the website to function and cannot be switched off. They are usually only set in response to actions made by you which amount to a request for services, suchas setting your privacy preferences, logging in or filling in forms. You can set your browser to block oralert you about these cookies, but some parts of the site will not then work. These cookies do not store any personally identifiable information.

Analytics

These cookies and scripts allow us to count visits and traffic sources, so we can measure and improve the performance of our site. They help us know which pages are the most and least popular and see how visitors move around the site. All information these cookies collect is aggregated and therefore anonymous. If you do not allow these cookies and scripts, we will not know when you have visited our site.

Embedded Videos

These cookies and scripts may be set through our site by external video hosting services likeYouTube or Vimeo. They may be used to deliver video content on our website. It’s possible for the video provider to build a profile of your interests and show you relevant adverts on this or other websites. They do not store directly personal information, but are based on uniquely identifying your browser and internet device. If you do not allow these cookies or scripts it is possible that embedded video will not function as expected.

Google Fonts

Google Fonts is a font embedding service library. Google Fonts are stored on Google's CDN. The Google Fonts API is designed to limit the collection, storage, and use of end-user data to only what is needed to serve fonts efficiently. Use of Google Fonts API is unauthenticated. No cookies are sent by website visitors to the Google Fonts API. Requests to the Google Fonts API are made to resource-specific domains, such as fonts.googleapis.com or fonts.gstatic.com. This means your font requests are separate from and don't contain any credentials you send to google.com while using other Google services that are authenticated, such as Gmail.

Marketing

These cookies and scripts may be set through our site by our advertising partners. They may be used by those companies to build a profile of your interests and show you relevant adverts on other sites. They do not store directly personal information, but are based on uniquely identifying your browser and internet device. If you do not allow these cookies and scripts, you will experience less targeted advertising.