The third quarter finished with robust gains for equities and fixed income alike despite some volatility along the way. The long awaited and highly telegraphed start of the Federal Reserve’s interest-rate cutting cycle began in September. U.S. 2nd quarter real GDP was revised higher by the Bureau of Economic Analysis, with the third estimate showing the economy grew at a seasonally adjusted annualized rate of 3.0%. The September non-farm payrolls report showed 254k jobs were added month-over-month, well above the consensus estimate of 150k. The U-3 unemployment rate decreased slightly in September to 4.1%. While this remains low from a historical perspective, it is above the 36-month moving average of 3.8%. Other economic data continued to provide mixed signals. The September ISM Manufacturing PMI was below 50, at 47.2, indicating contractionary territory. August retail sales came in stronger than expected as headline retail sales grew 0.1% month-over-month relative to a consensus estimate of negative 0.2%.

The Federal Open Market Committee (FOMC) announced a cut of 50 basis points to the target federal funds rate at its September meeting, bringing the target range to 4.75% – 5.00%. The size of the cut came as a surprise to many market participants. At the post-meeting presser, Fed Chair Powell defended the size of the cut as a “commitment to make sure the FOMC does not fall behind.” The meeting minutes indicated that a majority of the committee’s voting members expect additional cuts before year-end.

The European Central Bank delivered a 25-basis point cut to its deposit rate in September, the second such cut this year. This latest cut was widely anticipated, with the market more focused on any indication from the Governing Council on the future path of the rate cycle. China announced a stimulus package in late September in an attempt to pull its economy out of a deflationary trajectory. The package offers more funding and interest rate cuts intended to restore confidence after a series of disappointing data raised concerns of a prolonged structural slowdown. The Bank of Japan held its policy rate steady at its latest meeting. Its policymakers discussed the need to move slowly in raising rates amidst concerns over the outlook of the U.S. economy following the Fed’s 50-bps cut.

Performance

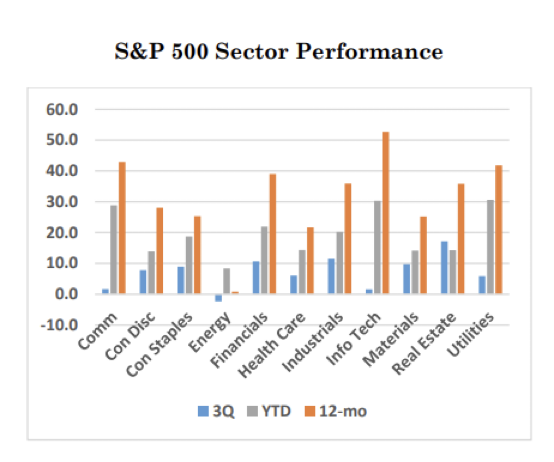

Stocks ended the quarter higher despite some turbulence, including a brief but sharp sell-off in August. The S&P 500 posted its fourth consecutive quarterly gain and ended September near an all-time high. Despite the volatility, the S&P 500 set multiple new all-time highs during the quarter. However, it was the change in stock market leadership that made headlines. The Equal-Weighted S&P 500, the Russell 2000, and the Value factor all outperformed the S&P 500, while the Growth factor underperformed. A similar pattern occurred at the sector level, with underperformers from the first half of the year outperforming in the third quarter. Interest-rate-sensitive sectors outperformed in anticipation of rate cuts, with the Utility and Real Estate sectors both gaining over +17%. Cyclical sectors, including Industrials, Financials, Consumer Discretionary, and Materials, also outperformed the S&P 500. In contrast, the Technology sector lagged the market rally, ending the quarter flat after outperforming in the first half of the year.

S&P 500 Sector Performance

Investors can look to two prominent events during the quarter to explain the sector rotation. During the first half of the year, uncertainty surrounding Fed policy and concerns about the economy pushed investors toward large-caps and AI stocks. At the same time, smaller companies lagged under the weight of higher interest rates. Fast-forward to Q3, and the Fed’s rate cutting cycle is underway and suddenly investors are questioning how long it may take to monetize the benefits of AI.

International

International markets performed strongly in Q3, with the MSCI EAFE Index up 7.26% and the MSCI Emerging Markets Index up 8.72%. Most regional indices worldwide were positive for the quarter, with Asian regional indices leading the way. China was a standout performer in Asia as a late-quarter rally boosted stocks in that country. After a brief mid-quarter sell-off, Japanese equities also ended the quarter in positive territory. European equities, including stocks in the United Kingdom, were also broadly positive.

In the wake of the Fed rate cut, several other major global central banks cut rates, too, including the European Central Bank, Swiss National Bank, and, notably, the People’s Bank of China. The Bank of Japan, which has only recently lifted the country out of its long-standing negative rates regime, increased rates from 0.1% to 0.25% in late July as it attempts to balance nascent inflation after years of deflation, a markedly weaker yen and lackluster economic growth.

Global monetary policy has been and will likely continue to be supportive after years of tightening, which could bode well for international equities. However, the pace of recovery remains uncertain in many regions, and there are risks that inflation may spike again, potentially undermining efforts to boost growth.

Commodities

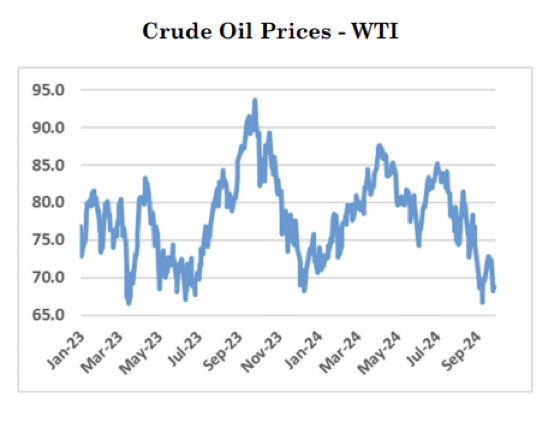

The Bloomberg Commodity Index delivered a gain for the third quarter. After a global growth scare in July and early August, commodities recovered in September as the Fed lowered interest rates and China implemented a series of large monetary and fiscal stimulus actions in an effort to revive its stagnant economy.

Within the Bloomberg Commodity Index, three of the four primary sub-complexes provided gains. Precious metals led results as slower growth, falling interest rates, a weaker US dollar and ongoing geopolitical tensions led the price of gold to a series of all-time highs during the quarter. Agriculture also closed the quarter with gains due to a September rally triggered by the weaker dollar and negative weather effects on coffee and sugar production. Similarly, a September rally in industrial metals helped copper, aluminum, nickel and zinc recover from early quarter losses as China’s policy stimulus efforts turned the tide. Energy declined as the sub-complex was simultaneously hit by apparent concerns that slowing growth would reduce demand and fear that OPEC would reverse voluntary production cuts, leading to oversupply.

Crude Oil Prices – WTI

Fixed Income

In Q3, fixed income investors experienced a little bit of everything. It started with some relatively dovish comments following August’s FOMC meeting, with Chair Powell laying the groundwork for future rate cuts. Unlike anything we’ve seen since the early days of COVID, early August saw a spike in volatility due to a culmination of events. The previously mentioned Bank of Japan rate increase was viewed as a hawkish move that contributed to a strengthening yen. A lower-than-expected non-farm payroll report for July and expectations for a more dovish move from the Federal Reserve fueled the unwind of the yen carry trade, wreaking havoc on the equity markets.

The volatility, however, was short-lived. Stronger than-expected US economic data (robust retail sales, falling CPI) and a relatively dovish Jerome Powell speech at Jackson Hole helped stabilize markets. Even the annual Bureau of Labor Statistics revision on August 21 of the prior year’s (Apr ’23 – Mar ’24) nonfarm payroll numbers was not enough to upend the market after the early volatility in August. The preliminary estimate of the revision indicated an adjustment of -818,000, an eye-watering and potential market-shaking event, but not so much. After August’s uncertainty, the calendar turning over to September was a welcome sign. For the first time in a long time, markets were uncertain as to what actions the Federal Reserve would take at its upcoming meeting.

September performance in fixed income markets (Bloomberg US Aggregate Bond Index, +1.34%) put the finishing touches on one of the best quarters of performance for the overall fixed income market in quite some time. The FOMC also released the most recent iteration of the dot plot, a chart that illustrates Fed expectations for future rate cuts. Expectations for the remainder of ‘24 include an additional 50 bps in cuts, split between the November 7 and December 18 meetings, bringing the year-end fed funds rate to 4.375% (4.25 – 4.50% range). This contrasted with market expectations, as measured by fed fund futures, which indicated a year-end level of 4.125% (4.00 – 4.25% range).

Moving into the year’s final quarter, economic data points will carry more weight as the market works to interpret their impact on the Fed outlook and global geopolitical implications (US election, Ukraine-Russia conflict, Mid-East conflict).

Inflation

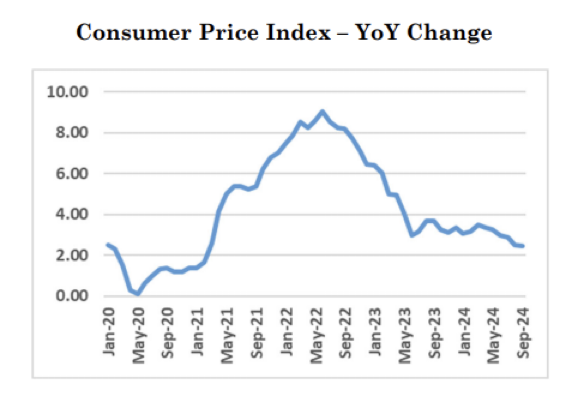

As mentioned above, the Fed began the process of lowering interest rates after a volatile five years. To recap, the Fed cut interest rates a total of 1.5% to near-zero during the COVID pandemic to support the economy. It kept rates near 0% until March ‘22, when it began raising interest rates in response to soaring inflation. From March ‘22 to July ‘23, the central bank raised rates by 5.25%, one of the largest and fastest rate-hiking cycles in decades. The Fed held interest rates steady for over a year as it waited for inflation to return to its 2% target, and after 14 months, it started the rate-cutting cycle with a 0.50% reduction at its September meeting.

The Fed’s transition to cutting interest rates comes as its focus shifts from lowering inflation to supporting the labor market. Since the last rate hike in July ‘23, annual inflation has dropped from 3.3% to 2.6%. However, over the same period, unemployment has risen from 3.5% to 4.2%, the highest level since October ‘21. The Fed appears confident that inflation will return to its 2% target but has expressed concerns about the health of the U.S. labor market. The Fed and investors are trying to understand the reasons behind, and impact of, the labor market softening over the past year. This could be the labor market simply normalizing after experiencing significant disruption during the pandemic. However, it may also be an early sign of weakening labor demand. This uncertainty is one reason the Fed moved to cut interest rates.

Consumer Price Index – YoY Change

Core CPI rose 2.4% for the twelve months ending September 30th while the index less food and energy rose 3.3% over the same time period. Index items that increased during the final month of the quarter include shelter, motor vehicle insurance, medical care, apparel and airline fares. Energy continues its overall downward trend over the past several months.

Fourth Quarter Insights

With the Fed beginning to lower interest rates, investors are focused on what happens next. The two key questions are how much the Fed will cut interest rates and how the economy will respond to those rate cuts. The next six months will be critical in providing answers to these questions, and investors will analyze each economic data point for clues about the economy’s trajectory. This intense focus on economic data may have the unintended consequence of keeping market volatility elevated as investors flip between optimism and pessimism.

Historically, the S&P 500 has performed very differently depending on whether the economy falls into a recession after the first rate cut. When rate cuts stimulate economic growth, the S&P 500 gains an average of +23% over the next 12 months. However, if a recession follows, the S&P 500 produces an average return of -4%. We will monitor economic data in the coming months to see what impact interest rate cuts have on the economy.

With the election quickly approaching, investors may be wondering how the outcome will affect financial markets and whether you should change your investment strategy. Political views can stir strong emotions, but making investment choices based on those feelings can lead to poor portfolio decisions. Data suggests that whichever party occupies the White House has little to no impact on investment performance, with fundamental factors like corporate earnings growth and valuations impacting the stock market far more than political headlines. The U.S. economy’s success, growth, and resiliency does not change with each new election, and neither should your long-term investment strategy.

Brian T. Moore, Vice President Trust Officer, Chesapeake Wealth Management

Published October 2024

References

1. S&P 500 Sector Return Data Morningstar: Third Quarter 2023 total return of ETF proxies.

2. Crude Oil Prices – WTI – Federal Reserve Economic Data: Year to date, crude oil prices, West Texas Intermediate.

3. CPI – Year over Year Change – Federal Reserve Economic Data: Year over year percentage change September 2023.

Disclaimer

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Chesapeake Wealth Management), or any non-investment related content, made reference to directly or indirectly in this newsletter, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Chesapeake Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his or her individual situation, he or she is encouraged to consult with the professional advisor of his or her choosing. Chesapeake Wealth Management is neither a law firm nor a Certified Public Accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Chesapeake Financial Group, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.

SEARCH

This here, it’s dependable and sealed tighter than a pickle jar, and it’ll pop up in a new window just to keep things tidy.