There was no shortage of market moving events in the fourth quarter. After a slow start in October, the election outcome triggered a broad rally in November. The rally faded in December, though the S&P 500 finished just slightly below its all-time high. The credit market was equally active during the quarter with the Federal Reserve cutting the fed funds rate by a combined 50 basis points. More importantly, the market now expects fewer rate cuts in 2025 relative to views held at the end of the third quarter. This resulted in a rather sharp rise in yields for longer dated Treasuries.

The U.S. economy continued to defy expectations last year, and has done so essentially from the time the Fed began raising interest rates in March of 2022. It was widely expected that the economy would slow as rates increased. To be sure, higher rates have affected housing demand and business investment. On the other hand, consumer expenditures have remained a steady driver of growth in recent quarters along with manufacturing construction. The controversial spending bills of 2021 have led to trillions in new spending on infrastructure, green energy, and other subsidies to incentivize domestic manufacturing. Everything from EVs, semiconductors, batteries, solar panels, and, of course, data centers have experienced a boom in production. Economic growth for 2025 is expected to slow a bit though it remains to be seen what effect the incoming Trump administration’s policies of extending the 2017 tax package, reduction of regulations across industries, and targeted manufacturing incentives will have.

Having begun with a 50-basis point cut in September, the Fed continued their rate cutting cycle with 25-basis point cuts at their November and December meetings. Both rate cuts were widely expected. The bigger development was the change in the outlook for 2025. Despite the two 4Q cuts, Powell and other regional Fed presidents indicated they are not in a hurry to cut rates further. The change in tone was the result of the economy’s recent strength. In turn, the market then re-evaluated its rate cut forecast. The clearest example of this was see in the divergence between the short end of the yield curve and the longer end. By quarter-end, the Fed had cut rates by 100 basis points. The 10-year Treasury yield, of which the market holds greater control, rose by nearly 100 basis points.

Performance

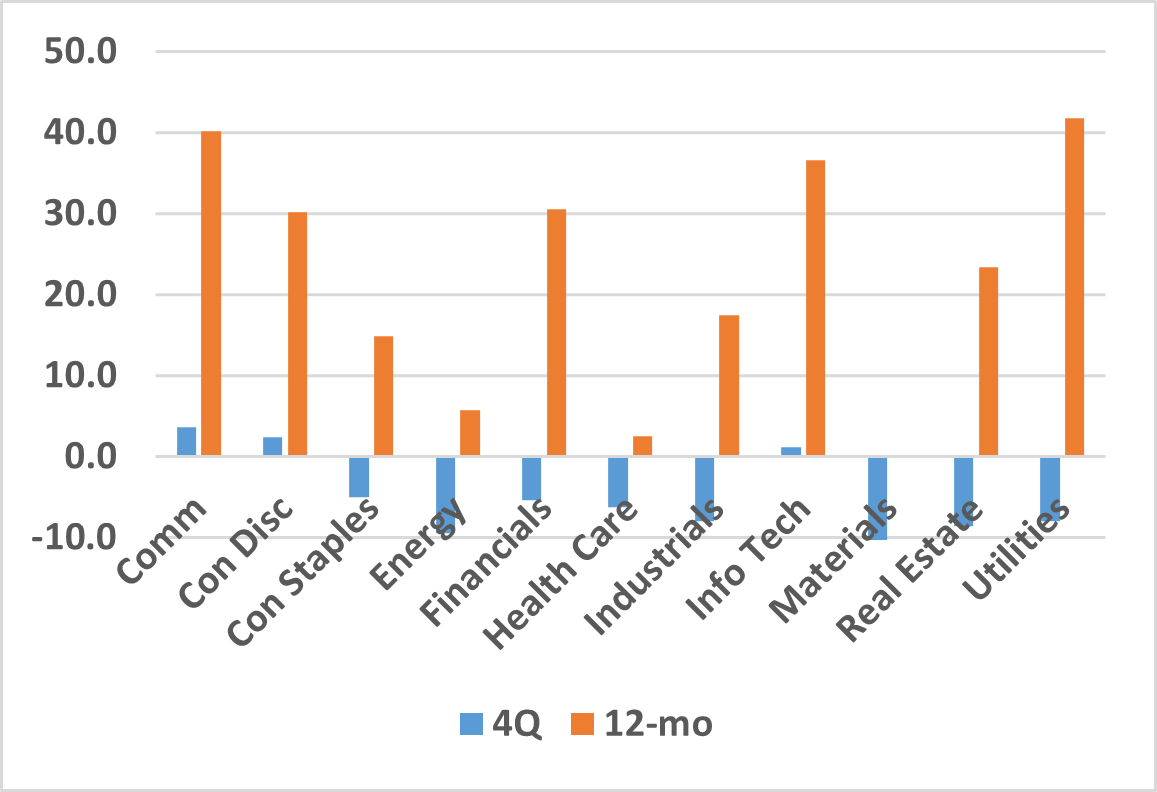

Looking more closely at the past year’s equity performance, the S&P 500 experienced consecutive years of +20% gains for the first time since the late ‘90s. Not coincidently, both time periods were largely driven by the technology sector. Breaking things down even further, the ‘Mag-7’ (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, & Tesla), combined to gain 63% for the year. The top 50 of the S&P 500 gained 32% compared to the total index return of 25% and the S&P equal-weighted return of 11%. Further down the capitalization scale, mid-caps returned roughly 15%, while small-caps gained approximately 12%. This concentrated rally, led by the aforementioned Mag-7, led to a rather unusual outcome. This year and last, fewer than thirty percent of the S&P 500 constituents outperformed the index return. This is well below the average of forty-nine percent going back almost twenty-five years.

S&P 500 Sector Performance

As mentioned earlier, the equity market experienced some volatility during the quarter. The sluggishness occurred as Treasury yields rose after the Fed’s first rate cut. The quick and decisive election outcome created a tailwind for stocks as investors anticipated an extension of the current tax policy, deregulation, and a U.S.-focused trade policy. Financials and Industrials both gained on these expectations. As the quarter came to a close, excitement cooled and many stocks that got a bump from the election began to trade sideways or took a negative turn.

International

European markets faced a wealth of challenges during the quarter, resulting in heightened economic and political instability. Surging energy costs, coupled with declining industrial output placed a strain on regional economies. The German automotive sector was a weak spot, with local manufacturers losing ground to Chinese EV competitors. Political instability further compounded these problems, as evidenced by no-confidence votes in both France and Germany. Trade policy uncertainties added another layer of concern with the incoming U.S. administration signaling possible new tariffs.

The Asia Pacific region displayed mixed results for the quarter with notable divergences among countries. The broader region, ex-Japan, declined primarily as a result of economic struggles in China. Despite Beijing’s attempts to boost growth through fiscal and monetary measures, persistent deflationary pressures and subdued consumer demand weigh on the market. South Korea faced even greater turbulence after parliament impeached President Yoon Suk Yeol in December.

Emerging markets were not spared from the downturn. A strengthening U.S. dollar and falling commodity prices placed pressure on resource-dependent economies, particularly in Latin America. Geopolitical instability further exacerbated market volatility. Regime change in Syria added to an already complex landscape that includes ongoing conflicts in Ukraine and the Middle East.

Commodities

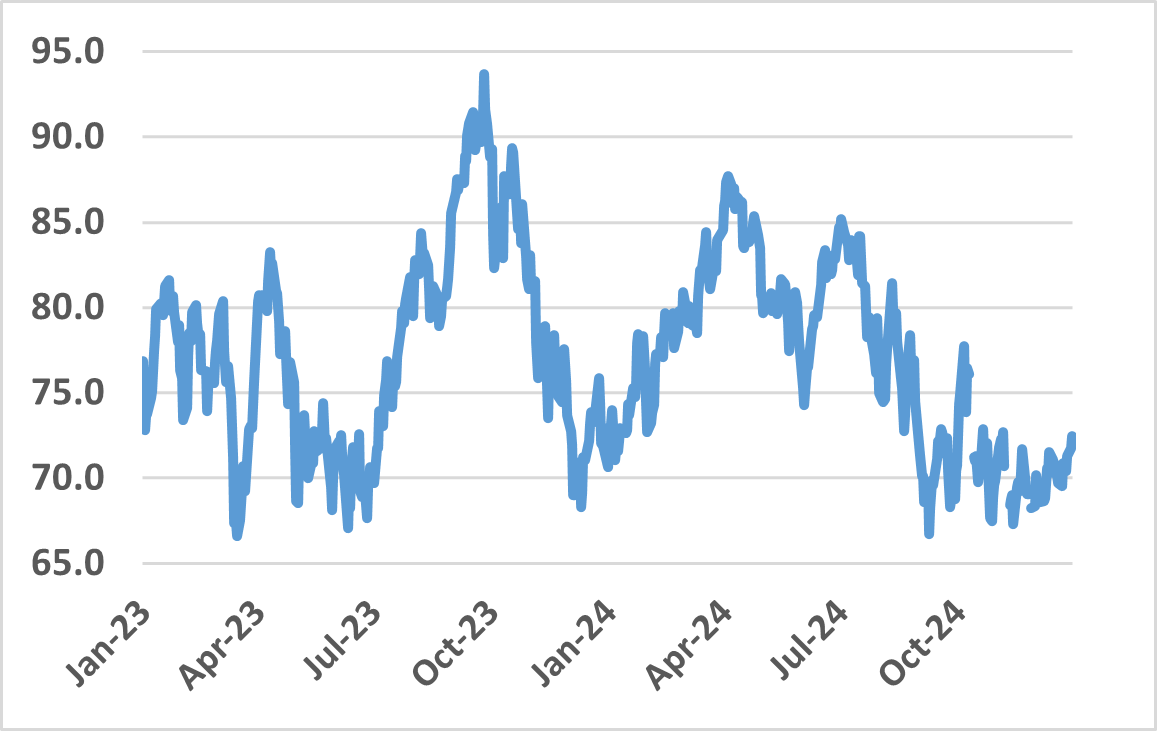

Commodities began the quarter with a poor start in October followed by gains in both November and December. Industrial metals declined largely due to comments made by the Federal Reserve which indicated a slower pace of rate cuts. Metals were also hampered by worry over President-elect Trump’s tariff policy and future demand from the renewable energy transition. Precious metals declined as the Fed’s guidance led to higher interest rates and a stronger dollar, causing gold to correct after hitting an all-time high of $2,800 an ounce in late October. Energy gains countered declines in other commodities as crude bounced up from the bottom of its trading range. Numerous catalysts drove oil, including China’s stimulus measures, OPEC extending its output cuts into 2025, regime change in Syria, and the ramp up of U.S. sanctions on Iranian and Venezuelan oil production.

Crude Oil Prices – WTI

Fixed Income

The sharp rise in Treasury yields weighed on bond returns during the quarter. The biggest differentiator within the bond market was duration, or the sensitivity of a bond’s price to changes in interest rates. Due to their lower duration, high yield corporate bonds were only slightly negative on the quarter. In contrast, investment-grade bonds were down roughly 4% as rising yields had a greater impact on their longer maturities.

Full year credit returns highlight the key themes that shaped the bond market throughout the year. Higher quality bonds such as U.S. Treasuries, Corporate investment-grade, and mortgage-backed securities underperformed as the market debated and ultimately lowered its rate cut expectations. In contrast, lower quality bonds outperformed as economic growth and corporate fundamentals remained solid. Corporate credit spreads, which measure the difference in yield between two bonds with similar maturities but different credit quality, steadily tightened throughout the year. While this provided a boost to lower quality bonds, it left credit spreads near their lowest levels in decades. In essence, this means investors are receiving less yield while taking on greater credit risk.

After fluctuating between zero and 20 basis points in October & November, the spread between the 10-year and the 2-year Treasury yields decisively widened to 30 basis points and broke previous highs. The shift was in response to data indicating a resilient labor market and stalled progress on disinflation. Agency mortgages, likewise, were caught up in the shifting yield curve. Aggregate prepayment speeds decreased late in the quarter, impacted by a rise in mortgage rates and negative seasonal housing factors. The 30-year mortgage rate, as measured by the Freddie Mac U.S. Mortgage Market Survey ended the quarter at 6.85%. In the corporate credit market, short-duration outperformed intermediate- and long-duration bonds. The better performing sectors include those involved in finance and banking while industrials, transportation, and utilities underperformed the broader corporate bond market.

Inflation

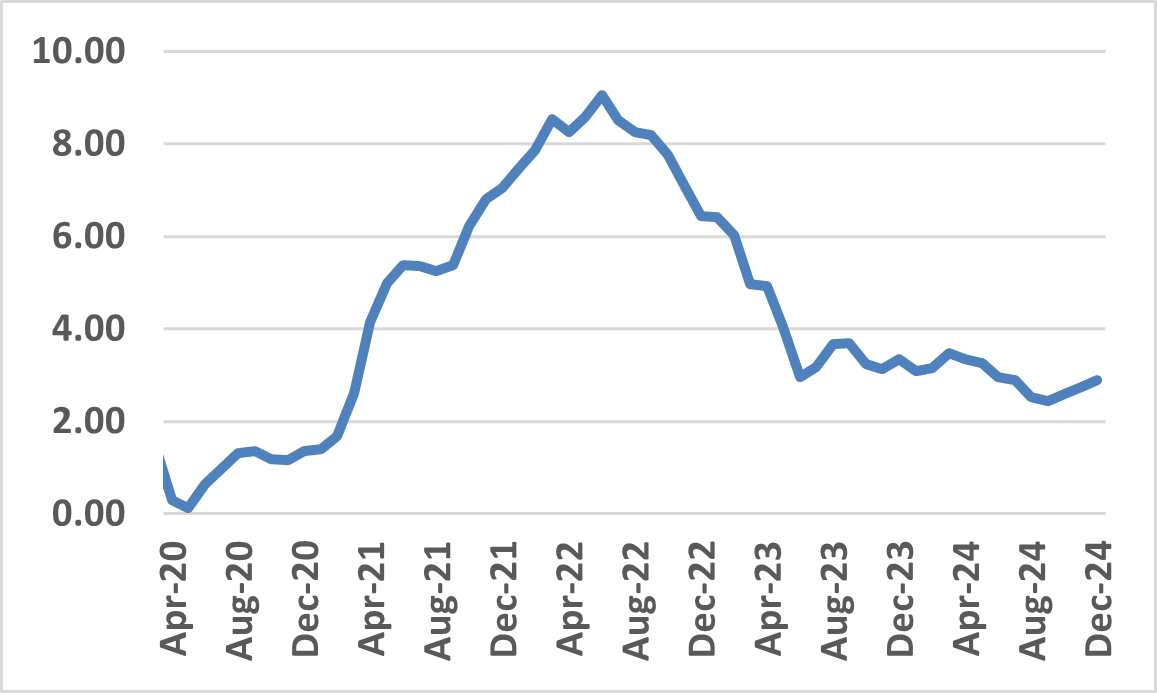

The Federal Reserve followed up its big September 50-bps reduction in the Fed Funds rate with more pedestrian 25-bps reductions in November and December. The December meeting saw the updated Summary of Economic Projections communicate that the Fed had reduced its estimate rate cut projections for 2025 from 100-bps to 50-bps. Continued stubborn inflation and a recovery in the labor market played a big role in the adjusted expectations. Chair Powell stated at his December press conference that the slower pace of rate cuts in 2025 “really reflects both the higher inflation readings we’ve had this year and the expectation that inflation will be higher”. The estimate also reflects that several of the FOMC members, likewise, foresee an uptick in inflation, along with higher growth and a stronger labor market. Looking ahead, investors will closely monitor the Fed’s ability to pull off the balancing act of setting a policy rate that is restrictive enough to ease inflation to the Fed’s 2% goal while not so restrictive that it boosts unemployment.

Consumer Price Index – YoY Change

First Quarter & 2025 Insights

The steady climb we witnessed in the S&P 500 this past year reflects a sense of growing confidence in the markets and the economy. Artificial intelligence and its potential epitomize this confidence. The economy outperformed expectations despite high interest rates. The market rally further intensified following the November election as investors focused on future tax policy, potential changes to the regulatory environment, and energy production. Some would even suggest this confidence has been echoed by the bond market in the form of some of the narrowest high-yield spreads in the last fifteen years.

Not nearly as discussed, however, has been the ever-increasing concentration in indices such as the S&P 500 that has occurred during this bull market. The debate currently taking place is whether or not this momentum can continue. The S&P 500 is currently trading at roughly 22x forward 12-month earnings. The few times the market has experienced these valuations occurred during the late-1990s technology boom and the more recent post-COVID recovery. Up to this point, investors have shown a willingness to pay these higher multiples. As this bull market matures, earnings growth and company fundamentals can be expected to play a larger role in determining the market’s path in the coming year.

In fixed income, it is anticipated that we will see mostly stable credit fundamentals while we navigate potentially higher yields, modestly wider spreads, and robust new-issue supply. In recent months, expectations for interest rate cuts have decreased significantly. Some pundits believe that the Fed may not cut rates at all in 2025. The 10-year’s recent upward trajectory can be attributed to investors’ demanding higher yields given increased uncertainty around economic growth and inflation, as well as expectations of higher deficits.

Brian T. Moore, Vice President Trust Officer, Chesapeake Wealth Management

Published January 2025

References

1. S&P 500 Sector Return Data

2. Crude Oil Prices – WTI – Federal Reserve Economic Data: Year to date, crude oil prices, West Texas Intermediate.

3. CPI – Year over Year Change – Federal Reserve Economic Data: Year over year percentage change.

Disclaimer

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Chesapeake Wealth Management), or any non-investment related content, made reference to directly or indirectly in this newsletter, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Chesapeake Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his or her individual situation, he or she is encouraged to consult with the professional advisor of his or her choosing. Chesapeake Wealth Management is neither a law firm nor a Certified Public Accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Chesapeake Financial Group, Inc.’s current written disclosure statement discussing our advisory services and fees is available upon request.

SEARCH

Welcome to the Login Menu.

You can access your account below.

It’s dependable and secure, and it will pop up in a new window in case you need to revisit the website.

We use information collected through cookies and similar technologies to improve your experience on our site, analyse how you use it and for marketing purposes.

We and our partners use information collected through cookies and similar technologies to improve your experience on our site, analyse how you use it and for marketing purposes. Because we respect your right to privacy, you can choose not to allow some types of cookies. However, blocking some types of cookies may impact your experience of the site and the services we are able to offer. In some cases, data obtained from cookies is shared with third parties for analytics or marketing reasons. You can exercise your right to opt-out of that sharing at any time by disabling cookies.

These cookies and scripts are necessary for the website to function and cannot be switched off. They are usually only set in response to actions made by you which amount to a request for services, suchas setting your privacy preferences, logging in or filling in forms. You can set your browser to block oralert you about these cookies, but some parts of the site will not then work. These cookies do not store any personally identifiable information.

Analytics

These cookies and scripts allow us to count visits and traffic sources, so we can measure and improve the performance of our site. They help us know which pages are the most and least popular and see how visitors move around the site. All information these cookies collect is aggregated and therefore anonymous. If you do not allow these cookies and scripts, we will not know when you have visited our site.

Embedded Videos

These cookies and scripts may be set through our site by external video hosting services likeYouTube or Vimeo. They may be used to deliver video content on our website. It’s possible for the video provider to build a profile of your interests and show you relevant adverts on this or other websites. They do not store directly personal information, but are based on uniquely identifying your browser and internet device. If you do not allow these cookies or scripts it is possible that embedded video will not function as expected.

Google Fonts

Google Fonts is a font embedding service library. Google Fonts are stored on Google's CDN. The Google Fonts API is designed to limit the collection, storage, and use of end-user data to only what is needed to serve fonts efficiently. Use of Google Fonts API is unauthenticated. No cookies are sent by website visitors to the Google Fonts API. Requests to the Google Fonts API are made to resource-specific domains, such as fonts.googleapis.com or fonts.gstatic.com. This means your font requests are separate from and don't contain any credentials you send to google.com while using other Google services that are authenticated, such as Gmail.

Marketing

These cookies and scripts may be set through our site by our advertising partners. They may be used by those companies to build a profile of your interests and show you relevant adverts on other sites. They do not store directly personal information, but are based on uniquely identifying your browser and internet device. If you do not allow these cookies and scripts, you will experience less targeted advertising.